Blog

QOF Lesser-of Rule: Why Your 2026 Gain Inclusion Needs a Real Appraisal

The QOF lesser-of rule caps your December 31, 2026 gain inclusion at the fair market value of your fund interest minus basis, not the deferred gain itself. This guide explains how that rule works and why it requires a defensible appraisal of an illiquid LP interest, not a guess at NAV.

Every investor who deferred a capital gain into a Qualified Opportunity Fund under the original Opportunity Zone regime faces the same date on the calendar: December 31, 2026. That is when the deferred gain comes due, whether or not the investor has sold anything. What determines the size of that tax bill is not simply the amount originally deferred. It is a statutory formula built around fair market value, and that formula is why a growing number of CPAs and fiduciaries are ordering appraisals of QOF interests well before year-end.

This article walks through what the "lesser-of" rule in IRC Section 1400Z-2(b) actually requires, why it forces a real valuation of an illiquid limited partnership or membership interest, and how discounts for lack of control and lack of marketability typically factor into that number.

What the Lesser-of Rule Actually Says

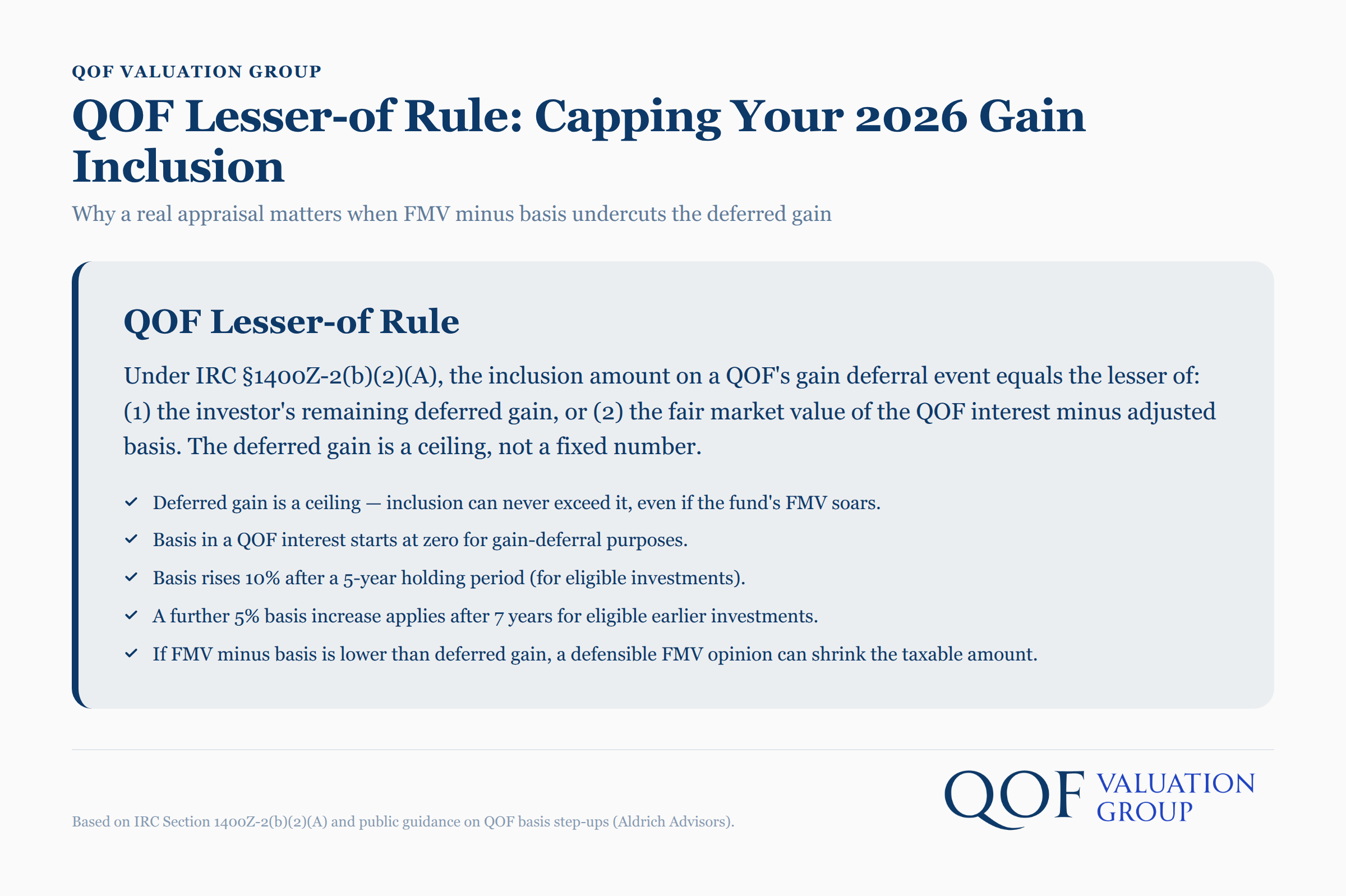

The amount a QOF investor must include in income on the inclusion date is the lesser of two figures: the investor's remaining deferred gain, or the fair market value of the QOF interest on that date minus the investor's adjusted basis in it. This is the operative mechanic under IRC Section 1400Z-2(b)(2)(A), and it means the deferred gain is a ceiling, not a fixed number.

If the fund has appreciated well beyond the original deferred gain, the investor still only includes the original deferred amount (adjusted for any basis step-up already earned). If the fund's fair market value has fallen, or basis has grown enough to close the gap, the includible amount can be smaller than the deferred gain, sometimes substantially smaller. That second scenario is exactly where a defensible fair market value opinion becomes valuable, because the investor is relying on that number to reduce a real tax liability.

Basis in a QOF interest generally starts at zero. Under the rules that applied to investments made in time to qualify, basis increased by 10% after a 5-year holding period, with a further 5% increase after 7 years for eligible earlier investments, a mechanism described consistently across public guidance on the 10% and 5% basis step-ups. Those step-ups directly reduce the amount subject to inclusion, because the formula nets fair market value against basis before comparing it to the deferred gain.

Key takeaway: the inclusion amount is capped by fair market value minus basis, not by the original deferred gain alone. When FMV minus basis is lower than the deferred gain, proving that FMV is not a formality. It is the entire basis for a smaller tax bill.

Why December 31, 2026 Still Governs Existing QOF Investments

December 31, 2026 remains the mandatory inclusion date for gains deferred into Qualified Opportunity Funds under the original Opportunity Zone regime (often called OZ 1.0), and nothing about that date changed for existing investors. The statutory inclusion event under Section 1400Z-2(b)(1)(B) was set when the original program was enacted, and it applies regardless of whether the investor has an exit event before then.

A new Opportunity Zone framework (sometimes referred to as OZ 2.0) was introduced through subsequent legislation, but that framework applies only to investments made on or after January 1, 2027. It does not reset, extend, or otherwise modify the inclusion date for gains already deferred under the original rules. If your firm's client rolled a gain into a QOF any time before that cutoff, the December 31, 2026 inclusion date still applies to them in full, and planning around it should already be underway.

Watch out: Don't let the headline noise about a "new" Opportunity Zone program create confusion with clients. The 2027-forward regime is a separate track. It has no bearing on the 2026 inclusion event for legacy investments.

Why This Rule Forces a Fair Market Value Appraisal

A QOF interest is almost never a publicly traded security with a quoted price. It is typically a limited partnership interest or an LLC membership interest in a fund holding real estate or an operating business, and there is no ticker, no daily closing price, and no ready market of buyers and sellers to reference. That is precisely the gap a professional appraisal is built to fill.

Determining the fair market value of that interest requires applying recognized valuation methodology: examining the fund's underlying asset values, its capital structure, distribution history, and the rights attached to the specific class of interest the investor holds. This is standard business and partnership interest valuation work, grounded in the same fair market value concept the IRS applies elsewhere in the tax code, and it should be prepared in accordance with the Uniform Standards of Professional Appraisal Practice maintained by The Appraisal Foundation.

Some QOFs do provide a semiannual net asset value calculation for purposes of meeting the fund's own 90% asset test, using either an applicable financial statement valuation or an alternative valuation method permitted under the Opportunity Zone regulations-1). That fund-level figure is a useful data point, but it answers a different question: whether the fund satisfies its own compliance threshold, not what a specific investor's minority interest is worth on the open market. Those two numbers are not interchangeable, and treating a fund's reported NAV per unit as automatically equal to the fair market value of an individual investor's interest is a common and costly mistake.

Applying Minority and Marketability Discounts to a QOF Interest

A QOF interest held by a passive limited partner or non-managing member is, in nearly every real-world case, a non-controlling and illiquid position, and that reality typically calls for two adjustments in the valuation.

- Discount for lack of control (DLOC): A minority interest cannot force a sale of fund assets, direct distributions, or control major fund decisions. Because that investor cannot compel the fund to act in ways that would unlock or accelerate value, appraisers typically apply a discount to reflect the reduced degree of control compared to owning 100% of the underlying assets outright.

- Discount for lack of marketability (DLOM): There is no established secondary market for most QOF interests. An investor cannot sell a partnership stake in a private real estate fund the way they could sell shares of a public stock, and that illiquidity is itself a value-reducing factor recognized broadly in business valuation practice, including in the Tax Court cases that have tested these discounts over time.

The combined effect of these two discounts is not a rounding error. Depending on fund structure, holding restrictions, and the investor's specific rights under the operating agreement, combined discounts of 20% to 40% off a pro-rata share of net asset value are common in minority, non-marketable interest valuations generally, and QOF interests are not exempt from that same logic simply because they originated as a tax deferral vehicle.

Pro tip: Ask your appraiser to document the specific rights (or restrictions) in the fund's operating agreement, transfer restrictions, redemption terms, and distribution policy. These are the facts that support the size of the discount applied, and they are exactly what a reviewer, whether an IRS examiner or opposing counsel, will look for first.

How Rev. Rul. 59-60 Factors Inform the Valuation

Revenue Ruling 59-60 remains the foundational IRS guidance for valuing closely held business interests, and its factors apply naturally to a QOF interest even though the ruling predates the Opportunity Zone program by decades. The ruling directs appraisers to weigh factors including the nature of the business, the economic outlook, book value and financial condition, earning capacity, dividend or distribution paying capacity, and the market for comparable interests.

For a QOF, this translates into an analysis of the fund's real estate or operating business holdings, its debt load, its historical and projected cash distributions to investors, and how comparable non-traded real estate or private equity interests have transacted. This is general industry valuation practice, not a QOF-specific methodology, and that consistency is itself a strength: it means the valuation stands on the same well-tested framework the IRS and courts have applied to closely held interests for over 60 years, rather than a novel approach invented for Opportunity Zone purposes.

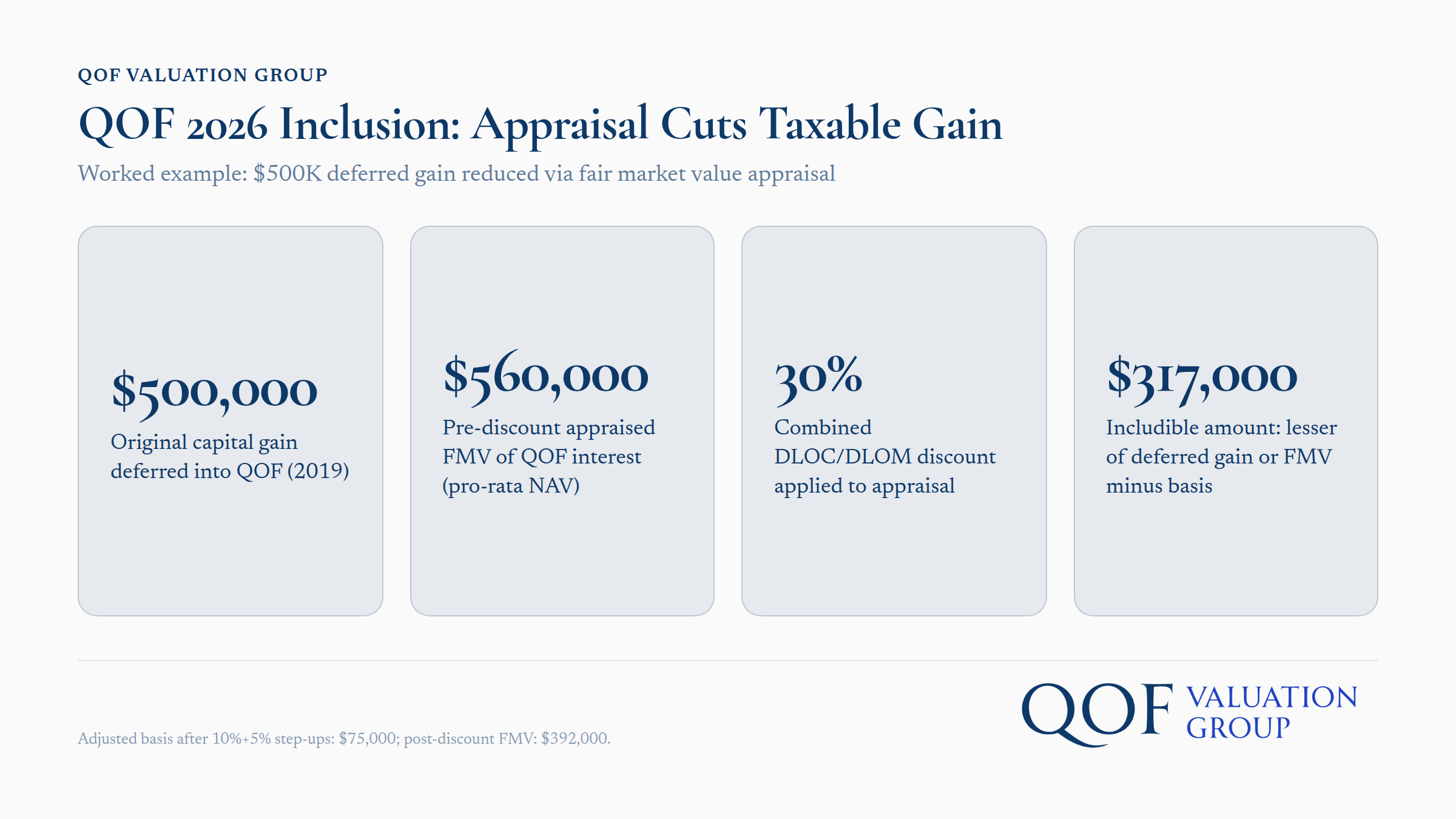

Worked Example: Deferred Gain vs. Fair Market Value vs. Basis

Consider an investor who deferred a $500,000 capital gain into a QOF in 2019, held it long enough to earn the available basis step-ups, and is now approaching the December 31, 2026 inclusion date.

| Figure | Amount |

|---|---|

| Original deferred gain | $500,000 |

| Basis step-up earned (10% + 5%) | $75,000 |

| Adjusted basis in QOF interest | $75,000 |

| Appraised fair market value of QOF interest (pro-rata NAV before discounts) | $560,000 |

| Less: combined DLOC/DLOM discount (30%) | ($168,000) |

| Fair market value after discounts | $392,000 |

| FMV minus basis ($392,000 - $75,000) | $317,000 |

| Includible amount (lesser of $500,000 deferred gain or $317,000) | $317,000 |

In this scenario, the appraisal supports an inclusion amount of $317,000 rather than the full $500,000 originally deferred, a difference of $183,000 in gain that is not subject to tax at the 2026 inclusion event. That gap exists entirely because the fund interest, once properly valued as a non-controlling, illiquid position, is worth less on a per-investor basis than a simple pro-rata share of the fund's asset value would suggest. Without a supportable appraisal, an investor has little basis to claim anything less than the full deferred gain.

Reporting the Inclusion on Form 8997

Investors in Qualified Opportunity Funds are required to file Form 8997 annually to report their QOF holdings, and the form must reflect the gain inclusion in the year it occurs. For most OZ 1.0 investors, that means the 2026 tax year return needs to show the deferred gain being recognized, calculated under the lesser-of rule described above.

The fair market value used to support that calculation should be documented at the time of the inclusion event, not reconstructed after the fact. An appraisal dated close to December 31, 2026, with a clearly stated valuation date and methodology, gives the return position something concrete to stand on if the IRS or a state taxing authority asks questions later.

Getting Your QOF Interest Valued Before the Deadline

The lesser-of rule rewards investors who can demonstrate, with a credible and well-documented appraisal, that their QOF interest is worth less than a simple share of fund NAV once minority and marketability factors are applied. Waiting until the final weeks of 2026 to start that process leaves little room for the fund-level diligence, discount analysis, and report preparation this kind of valuation genuinely requires.

Our team prepares fair market value appraisals of Qualified Opportunity Fund interests for the mandatory inclusion event, applying the same discount for lack of control and discount for lack of marketability analysis used throughout closely held business interest valuation, in accordance with USPAP. If you or your clients are holding a QOF interest facing the December 31, 2026 inclusion date, our Qualified Opportunity Fund valuation services can help establish a defensible fair market value well ahead of the deadline. You can also review our FAQ on qualified Opportunity Zones or explore how discounts for lack of control and marketability apply to a minority QOF interest in more depth, or request an appraisal directly to get started.

This article is provided for general informational purposes only and does not constitute legal, tax, or financial advice. Readers should consult a qualified attorney or CPA regarding their specific circumstances.